GST portal login process

Click here to open the GST gov portal this GSTIN portal; click on the login button in the menu bar (as shown below). The GST portal gives you a GST login form. Enter your username, password, and captcha code, and click on ‘Login.’ If you are a new user of the GSTIN portal, click on “click here” at the bottom of the login page. Take this GSTIN portal to the dashboard on successful login, where you can see a summary of your GST Credits, GST Payable (if any), Notices, etc.Commercial Tax:

Commercial Tax is an indirect tax and is generally imposed by the state govt on various products sold in that state. Commercial Tax is an imposition of Tax on the scheduled Commercial goods as indirectly collected by the seller or purchaser against his business transaction, which now comprises Sales Tax, Entertainment, Luxury Tax, and Entry. Tax and Profession Tax. GST replaced many taxes. This is one of the taxes, but on some commercial products, GST is not applicable, such as:Items Containing Alcohol:

Alcoholic beverages for human consumption would be kept out of the purview of GST as an exclusion mandated by constitutional provisions. Sales Tax/VAT could be continued to be levied on alcoholic beverages as per the existing practice. VAT is charged on alcohol purchases in some states, and there will be no objection. Excise duty, which is presently levied by the states, may also be unaffected.On Petroleum Products:

The full range of petroleum products, including crude oil and motor spirits, including Aviation Turbine Fuel (ATF) and High-Speed Diesel (HSD), would be kept outside GST, as is the prevailing practice in India. Sales tax could continue to be levied by the states on these products with the overall floor rate. Similarly, the Centre could also continue its levies. After further deliberations, we will issue a final opinion on whether we should keep natural gas outside the GST. As for petroleum products, although the GST constitutional amendment provides for levying GST on these products, it allows the time frame for their inclusion to be decided by the GST Council. Therefore, in the initial years of GST, petroleum products will remain out of the scope of GST. The taxation system under VAT and the Central Excise Act will continue for both commodities listed above. Calculate commercial taxes. Every state has Its commercial tax departments.GST Portal Login Guide.

India’s Goods and Service Tax (GST) portal is an official website hosted on www.gst.gov.in login https://www.gst.gov.in/. The GST Portal Login provides various services through which all the compliance activities related to Goods and Services Tax (GST) are undertaken by different entities. It offers additional services related to GST, like Goods and Service Tax registration and payment of taxes. GST master login also provides many relevant services, such as searching for the HSN code, locating the GST practitioner, filing of return and applying for a refund, etc., which can undertake through the GST login portal on gst.gov.in login and GST login India.

How Do I Sign Up for the GST Portal?

- Visit the website www.gst.gov.in login portal and make an application for registration under the new GST login with the help of the master India login guide.

- It would generate an acknowledgement number on submission of all the required details and documents.

- After completion of the verification process and on satisfaction through GST login, the GST officer issues the Goods and Service Tax Identification Number (GSTIN) on GST gov and the registration process is completed. This process will provide you with a username, and you can set a password of your choice for the GST portal India (www.gst.gov.in) dashboard.

How do you log in to the GST portal?

The GST Portal www.gst.login primarily serves two types of users:

- Existing Users

- New Users

Here is a complete master India GST login guide to the new GST portal:

In the case of existing users,

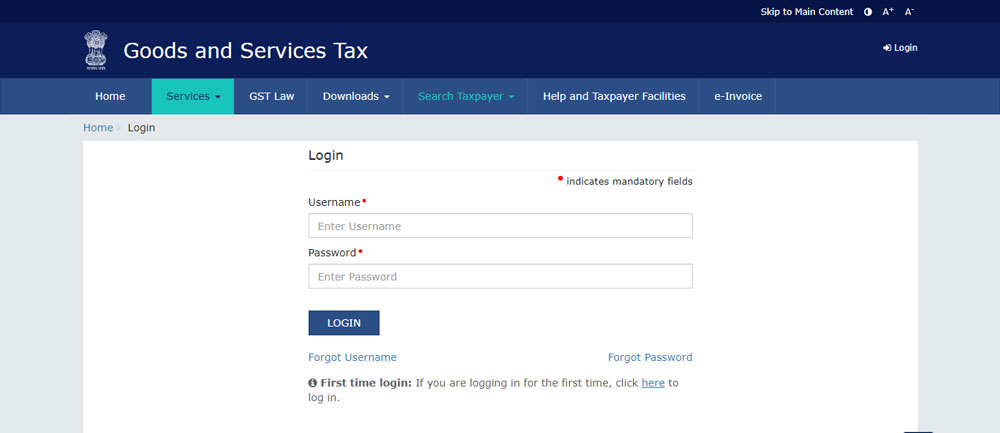

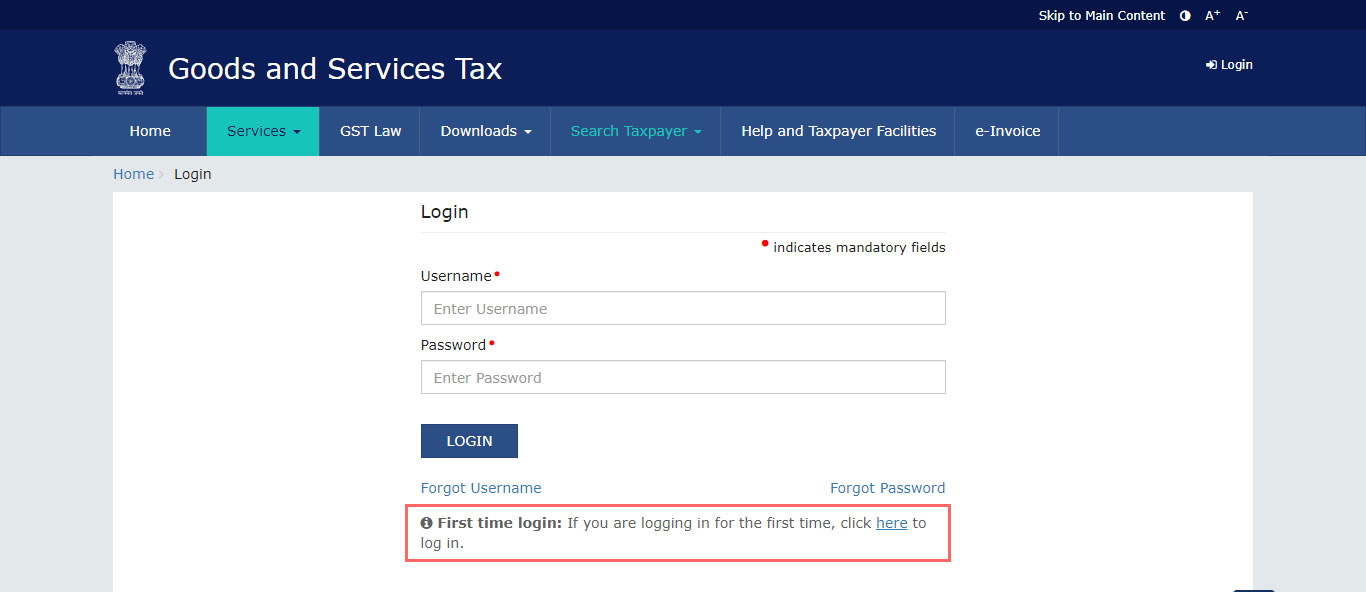

- Visit the website address www.gst.gov.in, select the Login icon on the top right corner of the homepage, and then enter the GST portal login password.

- Enter your username, password, and captcha code generated, and then click on “Log in” for GST login.

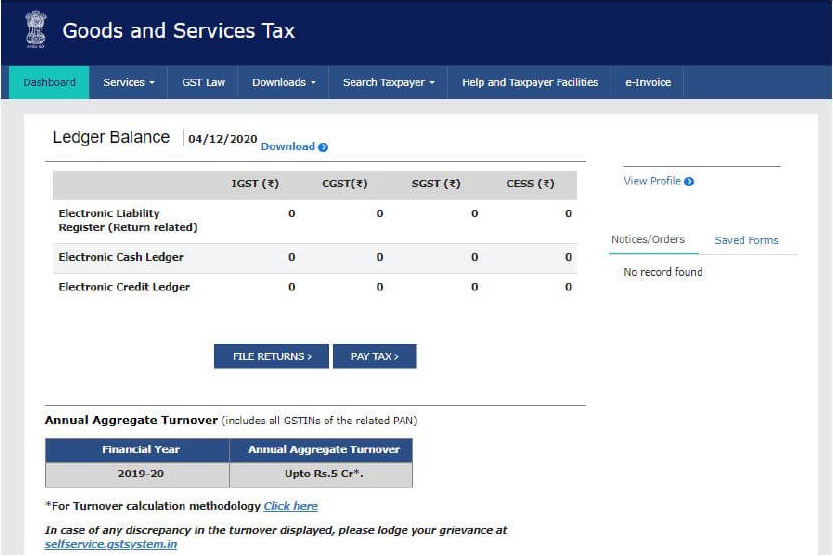

- On successful “GST Login,” you will be redirected to your dashboard on the GST portal. You can view the ledger balances of GST input tax credits that you have accumulated and the liability of tax in their respective heads: Electronic Liability Register, Electronic Cash Ledger, and Electronic Credit Ledger. Also, two tabs available on the screen are the “File Returns” tab and the “Pay Tax” tab. The dashboard also indicates the Annual Aggregate Turnover (AATO) and notices or orders from the GST department.

In the case of new users,

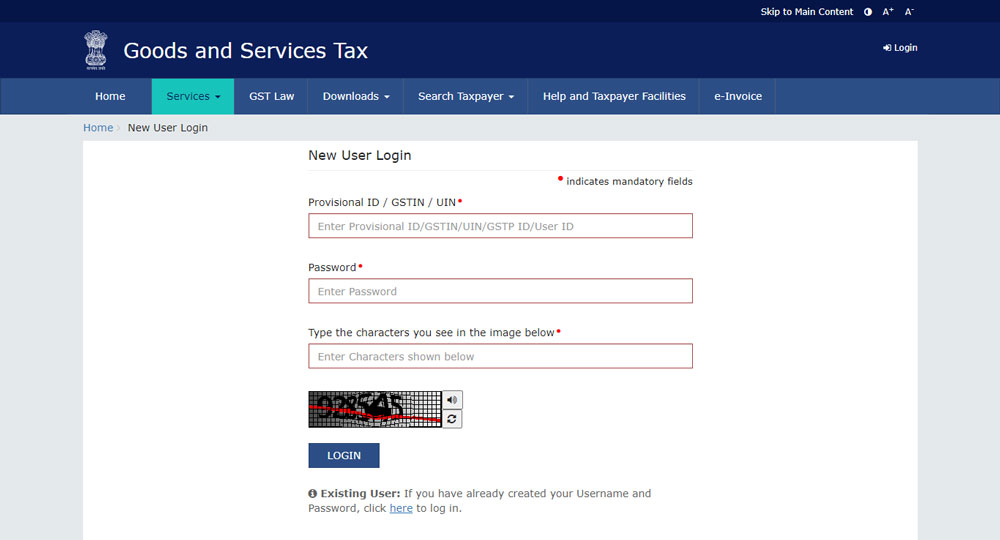

- Click on www.gst.gov.in and then click on the Login icon on the home page’s top right corner.

- Reach the end of the page on the right-hand side and then click on the word in the instructions given at the bottom of the page that states, “First time login: If you are logging in for the first time, click here to login.”

- Enter the allotted provisional ID/GSTIN/Unique Identification Number (UIN) and password you received at your e-mail address. Also, mention the generated captcha and click on the Login tab.

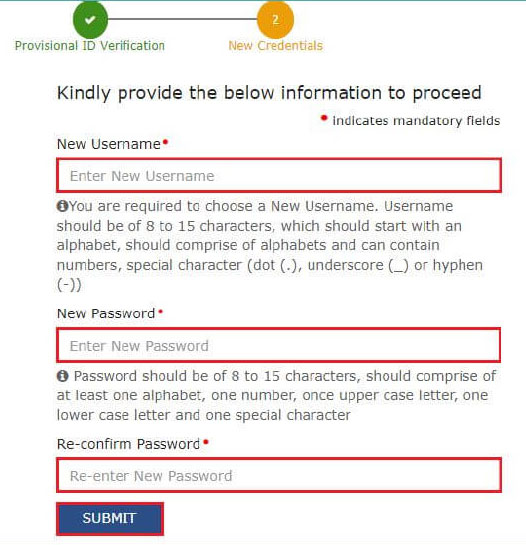

- You will be redirected to the new credentials page. Then input the username and password of your choice if available. Re-confirm the password again and then click on the Submit tab.

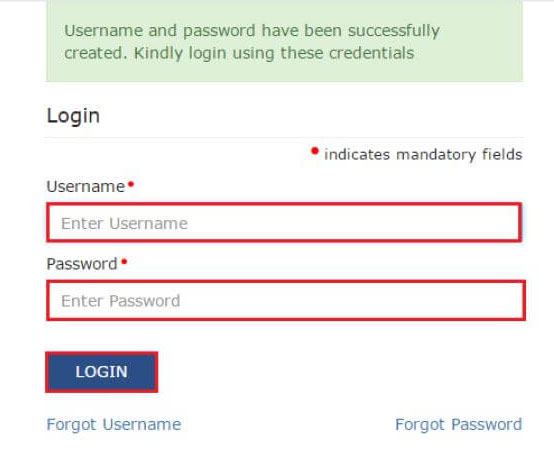

- On successful creation of the username and the password would be created. You can now successfully login into the GST Portal using these credentials created.

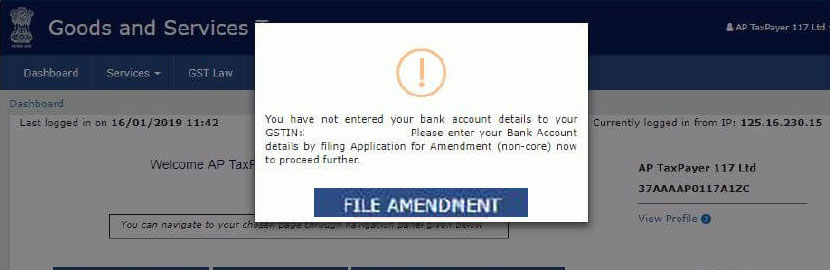

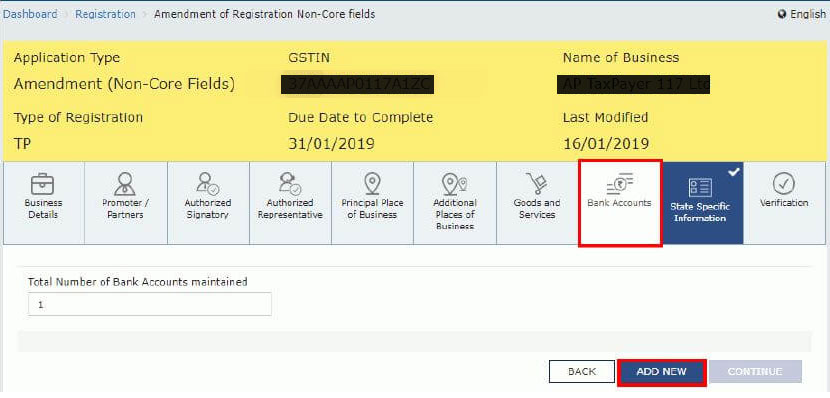

- Whenever you login into the GST Portal for the first time, you will be required to file an amendment application to submit the details of your Bank accounts. Then click on the FILE AMENDMENT tab.

- The application form would be available for editing and displayed on the screen. The non-core elements would be open for editing in the state. Edit the bank accounts column details by clicking the ADD NEW option button and applying.

Services available on the GST Portal

- Application for Registration as a Normal Taxpayer, a Casual Dealer, and an Input Service Distributor,

- Application for GST Practitioner appointment or as GST Practitioner,

- Application for Opting for a Composition Scheme,

- Application for Stock Intimation for the Composition Scheme Dealers

- Application for Opting out of the Composition Scheme System

- Filing of the Goods and Service Tax (GST) Returns,

- Payment of GST-CGST/SGST or UTGST/IGST

- claiming a refund of excess GST paid earlier,

- Furnishing of the Letter of Undertaking,

- The facility to view E-Ledgers,

- Filing of the Annual Return of GST,

- Application for Filing of the Reconciliation Statement

Who should get registered on the GST Portal?

- As per the GST Act, the following lists of individuals are essentially required to register on the GST Login Portal.

- Individuals who are previously registered under various taxation regime systems before the implementation of GST, such as VAT, Excise Duty, Service Tax, etc.

- All eCommerce aggregators require registration.

- Businesses in North-Eastern India, Manipur, Mizoram, Nagaland, and Tripura with an annual turnover of more than Rs. 10 lakhs.

- Companies in North-Eastern India, Arunachal Pradesh, Sikkim, Meghalaya, Uttarakhand, Puducherry, and Telangana with an annual turnover of more than Rs.20 lakhs.

- The input service distributors (ISD) and agents of suppliers

- Non-residents who are taxable and casual taxable persons

- Individuals who are required to pay tax under the reverse charge mechanism (RCM) and so on.

How to track the registration application status?

- Visit www.gst.gov.in, GST’s official website.

- Under the Services tab, select the Registration tab and choose Track Application Status.

- Select the ARN, input the ARN number, and click on the Search tab.

- Then kindly go through the instructions to view the current status of your application for registration.

How do I cancel my GST registration in the Portal?

- Visit www.gst.gov.in, the official website of GST.

- Click on “Login” and enter your User ID and Password to sign in.

- Click on the Services tab, the Registration tab, and select Application for Cancellation of Registration.

- Provide your official address and proceed with the Save and Proceed Option.

- Select the reason for the cancellation of your GST registration and then click on Save and Proceed.

- Cross-check the verification statement and provide the relevant details as required to be furnished. Verify your details using your Digital Signature Certificate (DSC) or the EVC option.

- Once the form is submitted, the applicant will receive the generated ARN number. You can keep it for future reference and communication.